Balance Sheet

There are three essential financial reports in any organization: the Balance Sheet, the Income Statement, and the Statement of Cash Flows. Although you may not be completely familiar with your organization’s financial statements, the purpose of the next section is to help you converse more easily with your finance staff, so together you can identify funding shortfalls or gaps.

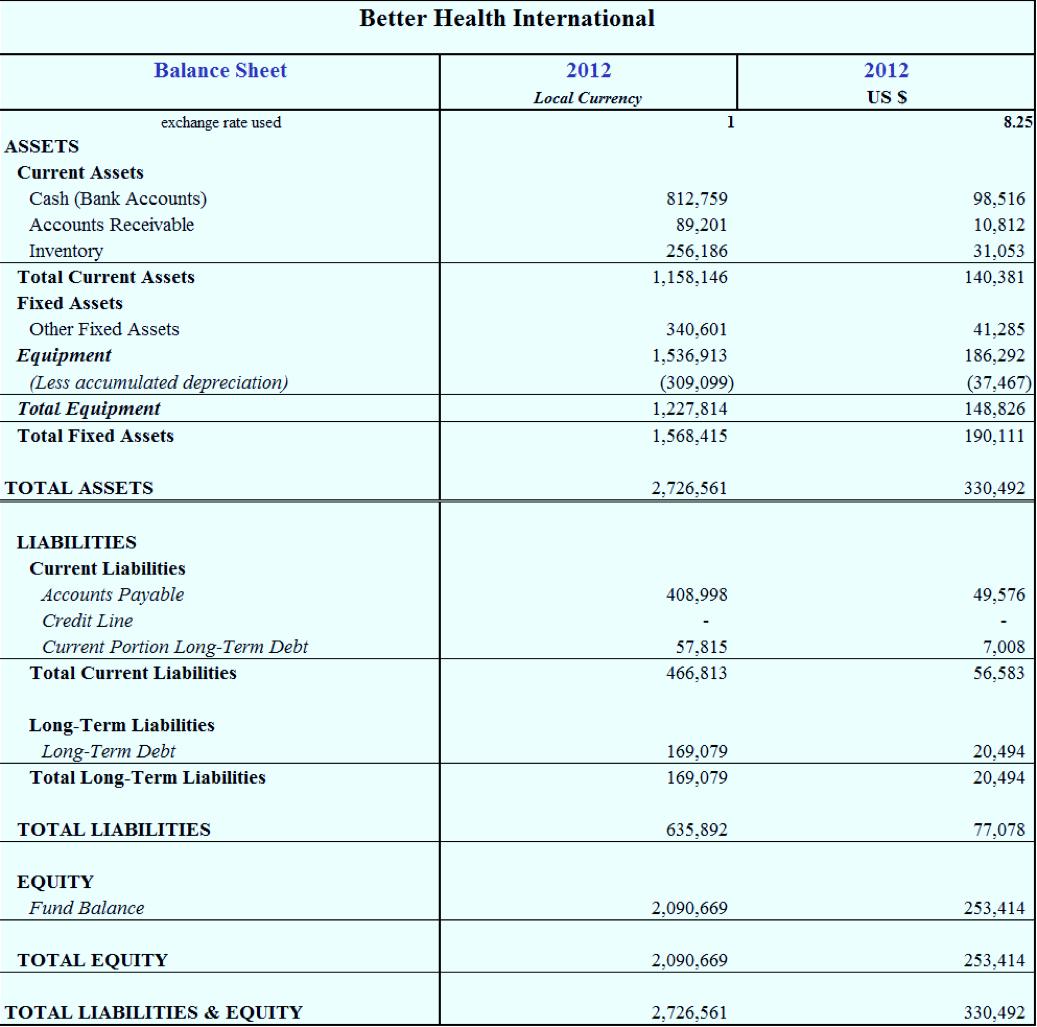

A Balance Sheet is always divided into two parts. The top half shows the organization's assets, while the bottom half shows the organization's liabilities and equity. The balance sheet can be understood as:

Equity + Liabilities = Assets

Sample Balance Sheet

The top and the bottom halves are always in balance; that is, they add up to the same amount. This is because the top half shows what the organization owns and what others owe the organization; while the bottom half shows what the organization owes and has to pay-out. The entries under each line of the balance sheet provide important information about the financial health of the organization.

In short, the Balance Sheet simply breaks all the financial and material assets into those that you own and those that you owe. They balance because the money that comes into your organization is often used to pay for services, salaries, benefits, inventory, etc. If there is money left over, it goes into your fund balance, or reserves, which, if not used in the fiscal year, often need to be returned to the donor or reinvested (spent on the organization). Therefore, any money that comes in will have a destination, which is why the balance sheet does, in fact, balance.